Buying a home is a significant milestone in anyone's life, and it often involves obtaining a mortgage to finance the purchase. One of the critical decisions you'll need to make is the down payment amount. Your down payment can have a substantial impact on your mortgage terms, monthly payments, and overall financial health. In this blog post, we'll discuss how to choose the right down payment for your mortgage.

Understanding Down Payments

Equity: Your down payment represents your stake in the property. The larger your down payment, the more equity you'll have in your home from day one. This can be essential for building wealth and ensuring financial stability.

Lower Loan Amount: A higher down payment means you need to borrow less money, which can lead to lower monthly mortgage payments.

Interest Savings: A smaller loan amount also translates to less interest paid over the life of the mortgage, potentially saving you thousands of dollars.

Qualification: Lenders often require a minimum down payment amount to qualify for a mortgage. Your down payment can affect your eligibility for different loan programs.

Now that we understand the significance of down payments, let's explore the factors to consider when deciding on the right amount for your situation.

The most critical factor in determining the appropriate down payment is your financial health. Consider your savings, income, and overall financial situation. Do you have enough cash on hand to make a substantial down payment without depleting your emergency fund or other savings? It's essential to strike a balance between a sizable down payment and maintaining a financial cushion for unexpected expenses. You must find out the highest and best use of your available assets.

Another crucial aspect to consider is your budget and monthly payments. A larger down payment will result in a lower loan amount and, consequently, lower monthly mortgage payments. This can make your homeownership experience more affordable and reduce financial stress. However, you must choose an amount that aligns with your budget and doesn't strain your finances.

Different types of mortgage loans have varying down payment requirements. For example:

- VA (Veterans Affairs) loans and USDA (U.S. Department of Agriculture) loans offer the possibility of zero-down financing for eligible applicants.

It's essential to research and understand the specific requirements for the type of mortgage you're considering. Keep in mind that some loans may have stricter criteria and require a higher down payment for borrowers with lower credit scores or unique financial situations.

Consider your long-term financial goals when deciding on a down payment amount. If you plan to stay in your home for many years and want to build equity over the long haul, a small down payment may be a route to consider. On the other hand, if you foresee a move in the near future, it may make more sense to put a little more down to account for any market adjustments and the costs to sell your home.

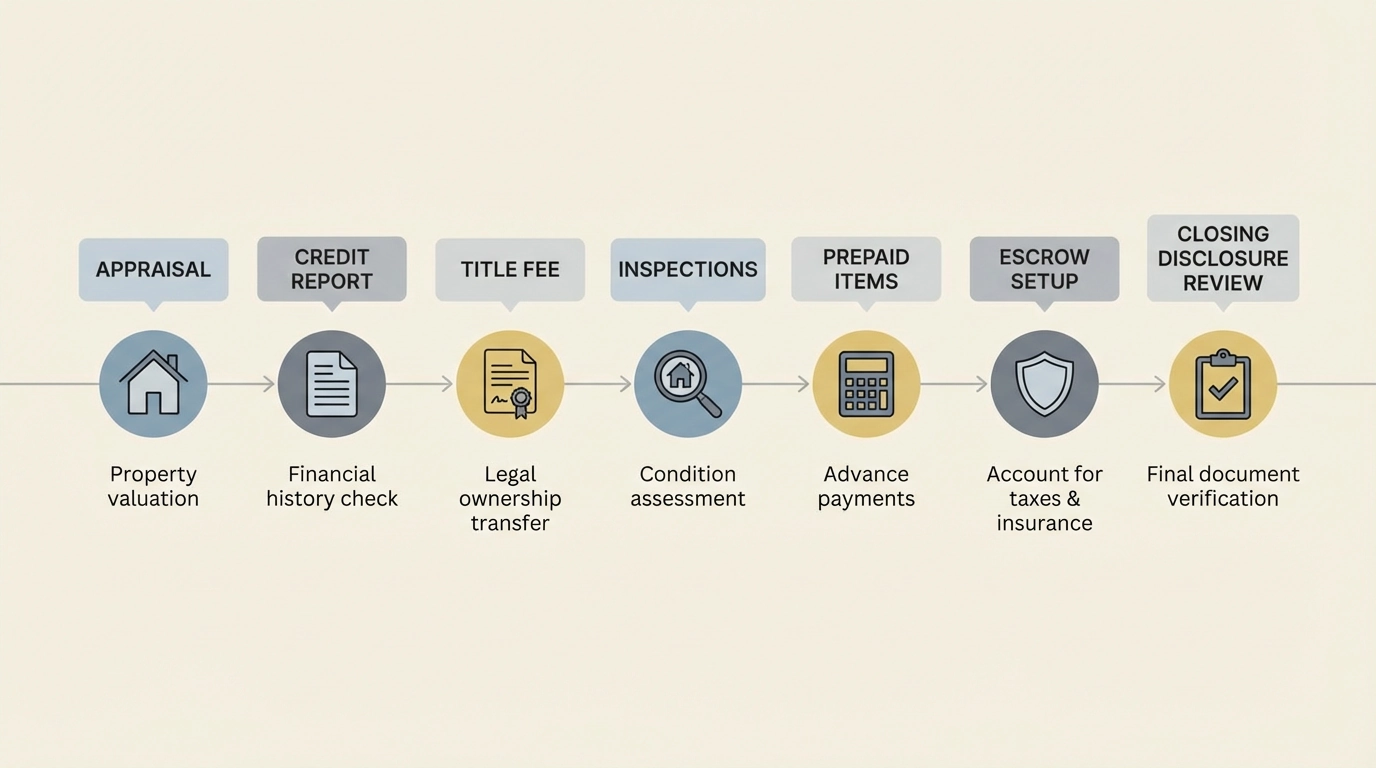

One key consideration tied to your down payment is mortgage insurance. If your down payment is less than 20% of the home's purchase price, most lenders will require private mortgage insurance (PMI) for conventional loans, or mortgage insurance premiums (MIP) for FHA loans. These insurance premiums can add to your monthly housing expenses. A higher down payment can help you avoid or reduce these additional costs.

Choosing the right down payment amount for your mortgage is a significant decision that can impact your finances for years to come. To make an informed choice, it's advisable to consult with a mortgage broker and financial advisor. They can assess your specific situation, explain the available loan options, and help you determine the optimal down payment based on your goals and circumstances.

To see how different amounts down can affect your payment, visit our online mortgage calculator.