A low mortgage rate gets attention. That makes sense. The interest rate affects the monthly payment and the long-term cost of the loan.

But the lowest rate is not always the best deal.

Mortgage pricing has tradeoffs. A lower rate may come with higher upfront costs. A slightly higher rate may come with a lender credit that lowers the money needed at closing. The right answer depends on the total cost, monthly payment, break-even point, and how long you expect to keep the loan.

That is why I like to compare mortgage options side by side. The rate matters, but it should not be the only thing driving the decision.

Mortgage Rates and Closing Costs Are Connected

Most borrowers think of the mortgage rate as one fixed number. In reality, there are usually several rate options available on the same loan. Each option has a different cost structure.

A lower rate may require discount points. A higher rate may provide a lender credit. The Consumer Financial Protection Bureau explains that discount points lower the interest rate in exchange for paying more at closing. Lender credits reduce upfront closing costs in exchange for a higher rate.

This is why two quotes can look very different. One may show a lower rate and higher cost. Another may show a higher rate and lower cost. Neither option is automatically better. You have to compare the full numbers.

What Are Discount Points?

Discount points are upfront fees paid to reduce the interest rate. One point usually equals 1% of the loan amount, but the rate reduction you receive for paying points can vary. It is not always a clean or guaranteed tradeoff.

For example, assume a buyer is borrowing $300,000. One discount point would equal $3,000. The borrower may pay that amount upfront to receive a lower interest rate.

This can make sense when the monthly savings are large enough and the borrower expects to keep the loan long enough to recover the upfront cost. It may not make sense if the borrower plans to sell, refinance, or pay the loan off in a short period of time.

What Are Lender Credits?

A lender credit works in the opposite direction. Instead of paying more upfront for a lower rate, the borrower takes a higher rate and receives a credit toward closing costs.

This can be helpful for buyers who want to preserve cash after closing. It can also help when cash to close is the bigger issue than monthly payment.

For example, a buyer may choose a slightly higher rate because it provides a lender credit that reduces closing costs by several thousand dollars. That could leave the buyer with more savings for moving expenses, repairs, furniture, or emergency reserves.

That does not mean the higher rate is always better. It means the upfront savings need to be compared with the higher monthly payment over time.

The Break-Even Point Matters

The break-even point helps compare a lower rate with a higher upfront cost.

Assume one option costs $4,000 more upfront and saves $100 per month. The simple break-even point is 40 months.

That means the borrower needs to keep the loan for a little over three years to recover the extra upfront cost through monthly savings.

If the borrower expects to keep the loan for 10 years, the lower rate may be worth serious consideration. If the borrower expects to sell or refinance within two years, paying the extra cost may not make sense.

This is one reason I do not like choosing a loan based only on the lowest rate. The lower rate may be the best long-term option, but only if the numbers support it.

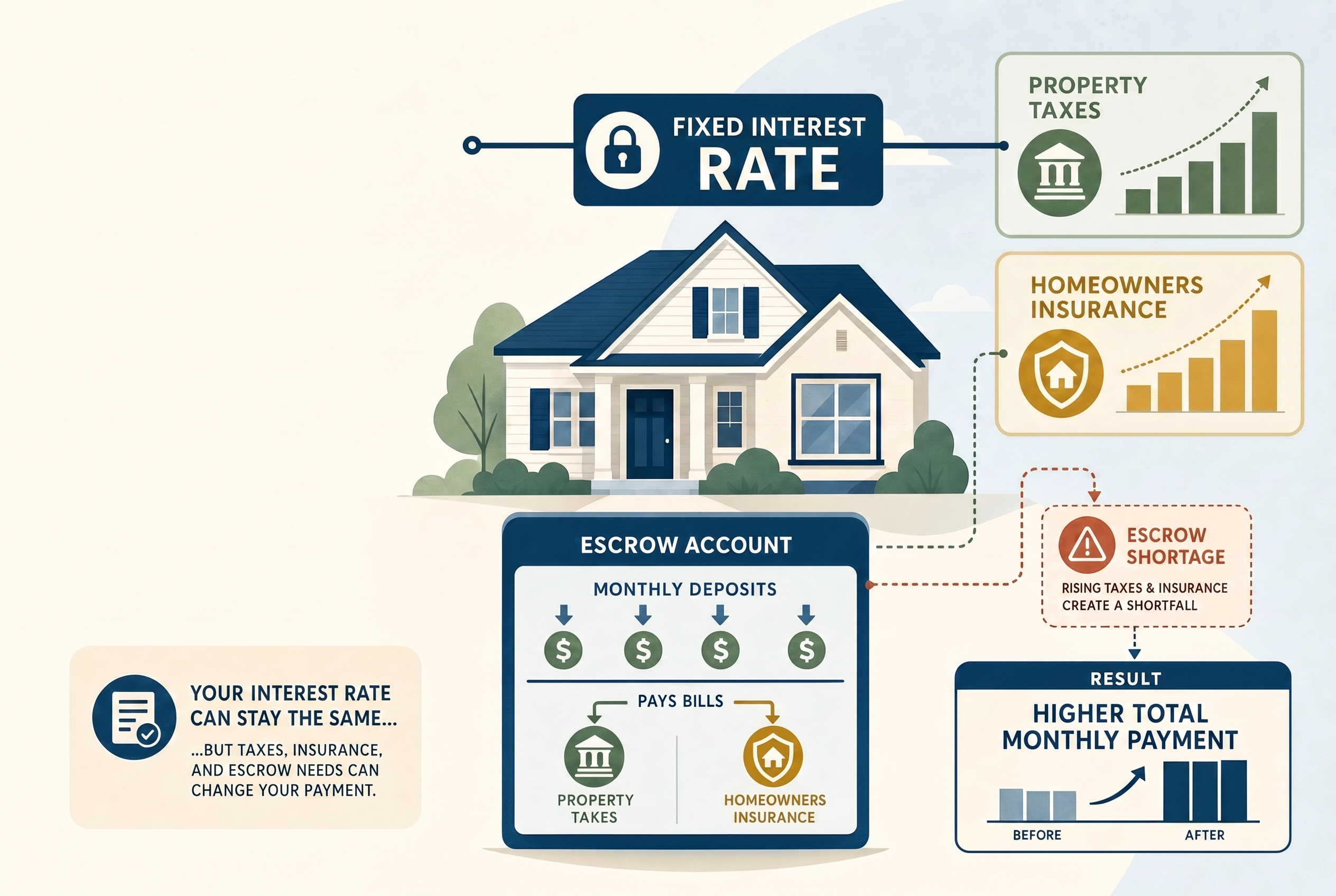

Compare the Total Payment

The interest rate affects the principal and interest payment, but the total mortgage payment can include other items too. Depending on the loan, the payment may include property taxes, homeowners insurance, mortgage insurance, and other escrowed items.

A loan with a lower rate may not always have the best total monthly payment if other parts of the structure are different. This can happen when comparing FHA and conventional financing, different down payment amounts, or options with different mortgage insurance costs.

This is especially important for buyers putting less than 20% down. Mortgage insurance can make a real difference in the payment. A lower interest rate with higher mortgage insurance may not be better than a slightly higher rate with lower mortgage insurance.

The full payment matters more than the rate by itself.

APR Can Help, But It Is Not Perfect

APR is another number borrowers see on mortgage quotes. APR is designed to show the cost of credit in a broader way than the interest rate alone. The CFPB explains that APR includes the interest rate plus certain loan costs.

APR can be useful, but I would not use it as the only decision tool. It assumes a certain way of spreading costs over time. Your actual result depends on how long you keep the loan.

For example, a loan with higher upfront costs may show a certain APR based on the full loan term. But if you sell or refinance after three years, your real-world cost may look different.

I prefer to look at the actual dollars. How much more does one option cost at closing? How much does it save each month? How long does it take to recover the cost?

Cash After Closing Is Part of the Decision

The best mortgage option is not always the one with the lowest payment. Sometimes keeping more money available after closing is more important.

This is common for first-time buyers. It can also matter for move-up buyers who need money for repairs, furniture, moving costs, or buy-before-you-sell transactions.

A buyer who spends every available dollar to get the lowest possible rate may end up with a lower payment but very little financial cushion. That can create stress after closing.

A slightly higher rate with lower upfront costs may be the better fit if it leaves the borrower with stronger savings. The right decision depends on the borrower's full financial picture.

Loan Term and Future Plans Matter

How long you expect to keep the home and loan should affect the rate decision.

If you plan to stay in the home for many years, paying more upfront for a lower rate may make sense. The monthly savings have more time to add up.

If you may sell, refinance, or pay down the loan in a few years, a lower-cost option may be better. The same is true if you expect to recast the loan after selling another home or use future funds to pay down the balance.

This is why a quote should not be reviewed in isolation. The loan should match the plan.

When the Lowest Rate May Be the Best Choice

The lowest rate may be the best choice when the borrower has enough cash, plans to keep the loan long enough, and the break-even point makes sense.

This can be a good fit for a buyer who wants to reduce long-term interest costs and has no concern about the extra upfront money. It may also fit a homeowner refinancing into a loan they expect to keep for many years.

The important point is that the decision should be based on the math, not the rate alone.

When a Higher Rate May Be the Better Choice

A higher rate may be the better choice when it comes with a lender credit or lower upfront cost that better fits the borrower's needs.

This may help a buyer keep more money in savings. It may also make sense when the expected time in the loan is short. If the borrower may refinance later, sell the home, or pay down the loan quickly, paying extra upfront for the lowest rate may not provide enough benefit.

This is not about choosing a worse loan. It is about choosing the structure that fits the situation.

Compare the Full Loan Before Deciding

The lowest mortgage rate can be attractive, but it is not always the best deal. The better comparison includes the rate, points, lender credits, closing costs, mortgage insurance, total payment, cash needed at closing, and break-even point.

At Capital City Mortgage, I like to show borrowers multiple options when it makes sense. One option may have the lowest rate. Another may have lower upfront costs. Another may land somewhere in the middle.

The right answer depends on the numbers and the borrower's goals. A good mortgage decision should make sense on paper and in real life.

Frequently Asked Questions

Is the lowest mortgage rate always the best option?

No. The lowest rate may come with higher upfront costs. It may be the best option if you keep the loan long enough to recover those costs, but it is not always the best fit.

What are discount points?

Discount points are upfront fees paid to lower the interest rate. They can reduce the monthly payment, but you should compare the upfront cost with the monthly savings.

What is a lender credit?

A lender credit reduces your closing costs in exchange for a higher interest rate. This can help lower the money needed at closing, but it usually increases the monthly payment.

How do I compare mortgage rate options?

Compare the interest rate, points, lender credits, lender fees, mortgage insurance, total payment, cash needed at closing, and break-even point. The best option depends on your goals and how long you expect to keep the loan.