Paying off debt before buying a house sounds like an obvious financial move. A lower debt balance can improve your monthly budget and may help you qualify for a mortgage. However, using all your available cash to eliminate debt is not always the best strategy.

Mortgage approval depends on more than the total amount you owe. The type of debt, required monthly payment, available savings, credit score, and loan program can all affect the answer.

Before paying off a car loan, credit card, or personal loan, it helps to review how the decision will affect your entire mortgage application.

Mortgage Lenders Focus on Monthly Payments

Mortgage lenders calculate a borrower’s debt-to-income ratio, commonly called DTI. This compares your required monthly debt payments to your gross monthly income.

For example, assume you earn $7,000 per month before taxes and have the following debts:

- $550 car payment

- $150 student loan payment

- $100 minimum credit card payment

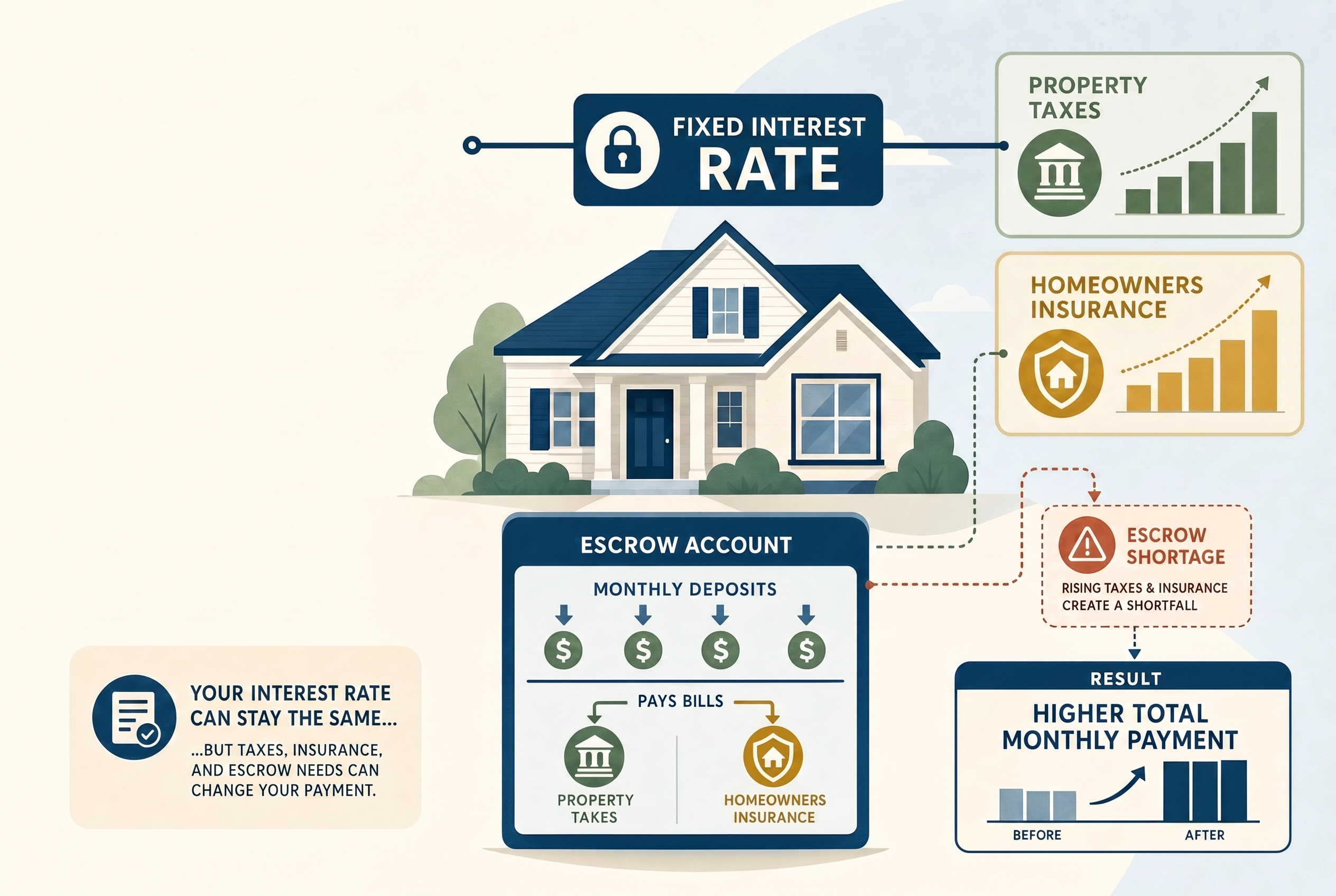

Your existing monthly debt payments total $800. The lender then adds the proposed house payment, including principal, interest, property taxes, homeowner’s insurance, mortgage insurance, and any homeowners association dues.

The monthly payment usually matters more than the total balance. A $20,000 car loan with a $600 payment can have a much larger impact on mortgage qualification than a $20,000 student loan with a $150 payment.

This is why paying off the debt with the largest balance is not always the most effective option.

Paying Off Debt Can Increase Your Buying Power

Eliminating a monthly payment can create more room for a mortgage payment. In some cases, paying off a relatively small balance can make a meaningful difference.

Suppose you owe $3,000 on a car loan with a $500 monthly payment. Paying off that loan could remove the entire $500 payment from your debt-to-income ratio. Depending on the loan program, interest rate, taxes, and insurance, that could potentially create room for a larger mortgage payment.

However, the same $3,000 may also be needed for your down payment, closing costs, emergency savings, moving expenses, or repairs after closing. Increasing your maximum approval does not automatically mean paying off the debt is the right move.

The goal should be to improve the overall loan plan, not simply qualify for the highest purchase price possible.

Do Not Overlook Your Cash Reserves

Cash is valuable during and after a home purchase. Buyers may need money for:

- The down payment

- Closing costs

- Homeowner’s insurance

- Property tax and insurance reserves

- Inspections

- Moving expenses

- Immediate repairs or improvements

- Emergency savings

Using most of your savings to pay off debt could leave you with very little financial cushion after closing. That can create more stress than keeping a manageable monthly payment.

Some mortgage programs also consider reserves as part of the overall application. Reserves are funds remaining after the purchase is complete. They are not always required, but having extra money available can strengthen a loan file, especially when the application includes higher debt ratios, multiple properties, variable income, or other risk factors.

Paying Off a Credit Card Can Affect Your Credit Score

Credit card debt is different from installment debt such as a car loan. Paying down credit cards can reduce your credit utilization ratio, which compares your balances to your credit limits.

Lower utilization can help improve a credit score. A higher credit score may help you qualify for better mortgage pricing, lower mortgage insurance, or additional loan options.

However, you should avoid closing the credit card account after paying it off unless there is a specific reason to do so. Closing an account may reduce your available credit and affect the age or structure of your credit history.

Credit scores can react differently depending on the borrower’s overall credit profile. It is usually better to review the expected impact before moving large amounts of money or changing accounts.

Should You Pay Off a Car Loan?

A car loan can significantly affect mortgage qualification because the monthly payment is often substantial.

Paying it off may make sense when the remaining balance is low and eliminating the payment improves your debt-to-income ratio. In certain situations, a car payment with only a limited number of payments remaining may be treated differently under mortgage guidelines. The exact treatment depends on the loan program and the effect of the payment on the borrower’s ability to manage the new mortgage.

Do not assume the payment will automatically be excluded because the loan is nearly paid off. The lender should review the account and determine how it must be handled.

Should You Pay Off Student Loans?

Student loans can be more complicated. The payment used for mortgage qualification may depend on whether the loan is in repayment, deferment, forbearance, or an income-driven repayment plan.

Conventional, FHA, VA, and USDA loans can have different requirements for calculating student loan payments. The payment appearing on your credit report may not always be the payment the lender must use.

Before making a large payment toward a student loan, ask how the current loan program will calculate the obligation. Paying down the balance without eliminating the required payment may provide little or no improvement to your mortgage qualification.

Paying Off Debt at Closing

In some cases, debt can be paid off as part of the mortgage closing instead of being paid before the application is complete.

This can protect the buyer from using money too early and then discovering that the transaction requires additional funds. It also gives the lender and title company a clear record of the payoff.

The lender may need a current payoff statement and proof that enough funds are available. Requirements vary based on the type of account and loan program.

Do not make this decision without coordinating with your mortgage professional. The payoff must be properly documented, and changes to your available assets can affect final loan approval.

When Paying Off Debt May Make Sense

Paying off debt before buying a home may be helpful when:

- The payment is preventing loan approval.

- A small payoff eliminates a large monthly obligation.

- Paying down credit cards could improve your credit profile.

- You will still have enough money for closing and emergency savings.

- The payoff could improve the interest rate or mortgage insurance cost.

- You want a lower overall monthly debt burden after buying the home.

The best debt to pay off is often the one that produces the greatest improvement while using the least amount of cash.

When Keeping the Debt May Be Better

Keeping the debt may be the stronger option when paying it off would use most of your available savings. It may also make sense when the monthly payment is small, the debt has a low interest rate, or paying down the balance will not change the payment used for qualification.

A buyer may be better off keeping $15,000 in savings than using the entire amount to pay down an installment loan that still has nearly the same monthly payment.

The decision should account for the mortgage approval and your finances after closing.

Review the Numbers Before Moving Money

Avoid paying off accounts, closing credit cards, transferring large amounts of money, or making major purchases while preparing for a mortgage without first discussing the change with your lender.

A good mortgage review can compare several options:

- Qualifying with the debts as they are.

- Paying off one or more accounts.

- Paying down revolving balances to improve credit.

- Reducing the purchase price.

- Increasing the down payment.

- Using a different mortgage program.

Sometimes paying off debt is the best answer. Other times, keeping the cash creates a safer and more flexible home purchase.

Capital City Mortgage helps Nebraska buyers compare these choices before they make major financial changes. We can review your income, debts, credit, available funds, and homebuying goals to build a loan strategy that works both at closing and after you move into the home.

Frequently Asked Questions

Does paying off debt increase how much house I can afford?

Paying off debt may increase your buying power if it eliminates a monthly payment used in your debt-to-income ratio. The actual improvement depends on your income, loan program, interest rate, taxes, insurance, and other debts.

Should I pay off credit cards before applying for a mortgage?

Paying down credit cards may lower your required monthly payments and improve your credit utilization. However, you should keep enough money available for the down payment, closing costs, reserves, and unexpected expenses.

Can I pay off a car loan at mortgage closing?

A car loan may be paid off at closing when the lender approves the arrangement and the payoff is properly documented. The lender will also verify that you have enough eligible funds to complete the payoff and the home purchase.

Should I close a credit card after paying it off?

Closing a credit card may reduce your available credit and could affect your credit score. Unless there is a specific reason to close the account, it is usually better to discuss the potential credit impact with your mortgage professional first.